Positive macroeconomic trends in January 2024 amid speculation regarding timing of rate cuts

The start of 2024 witnessed strength in the US equity market, speculation around the timing of rate cuts and growing geopolitical tensions.

The start to 2024 has seen a continuation of strength in the US equity market while other areas are still trying to find direction. Central banks remain in focus although the conversation has shifted from higher for longer to when do rate cuts start. There is an overarching concern about the various wars taking place globally and risk of escalation. With the recent Red Sea shipping attacks by Houthi rebels adding to these concerns and worries around the US being drawn further into the conflict in the Middle East following a drone attack killing three US soldiers.

Generally, the macroeconomic data in January supported the goldilocks narrative that the market has been hoping for as the US GDP growth came in stronger at 3.3% which was well ahead of expectations of 2%. This was backed up by labour and housing data. Inflation was slightly mixed with December CPI coming in at 0.3% m/m which was slightly hotter than the 0.2% consensus. This was driven by higher new vehicle sales and apparel and shelter remains a bit sticky. On the other hand the December PPI reading confirmed the disinflationary trend and this was further backed up by the Fed’s preferred inflation reading being PCE.

China was also in the news with rumours authorities were looking to support the slumping stock market which some participants saw as positive. Unfortunately, Evergrande the beleaguered property company was placed into liquidation and there are concerns around the potential contagion effect for China.

South Africa’s MPC kept rates on hold and indicated that they don’t see any rate cuts in the short term despite inflation coming in lower than expected. There are significant concerns around South Africa’s crumbling infrastructure and the latest focus is on Transnet and the far reaching consequences for a number of industries from miners to retailers. We can also expect a ramp up in political noise in the coming months leading up to the election. This is already evidenced by former president Jacob Zuma starting his own political party resulting in his suspension from the ANC.

Should current macro data trends continue then the macroeconomic backdrop looks to improve globally however geopolitical tensions and a record number of elections will still drive a lot of volatility during 2024.

Macro environment

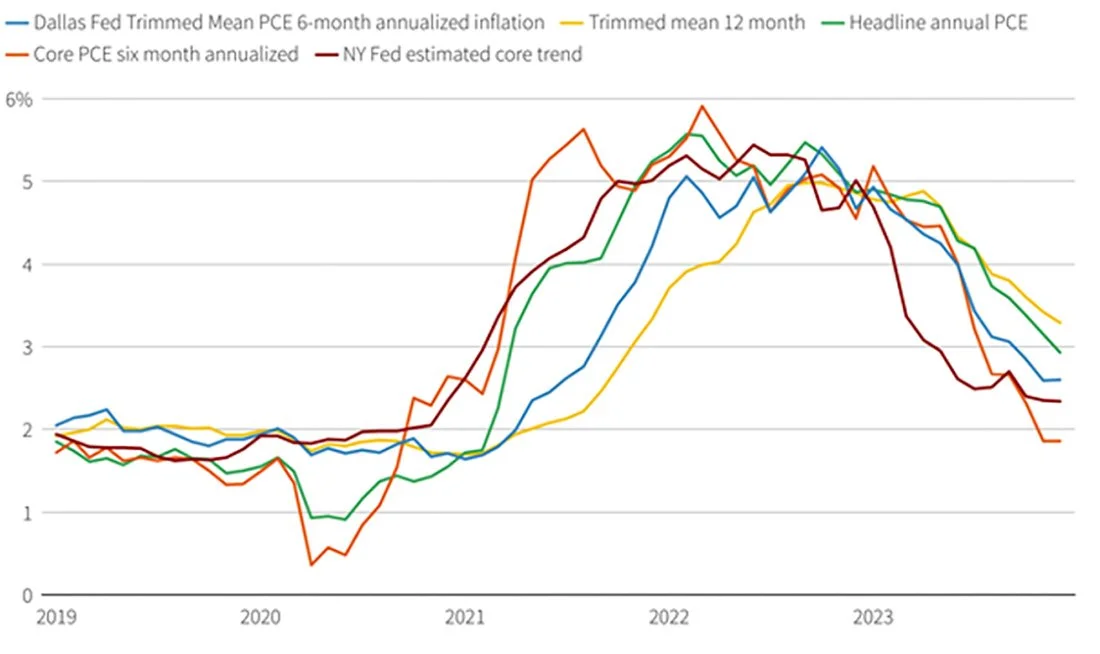

2024 has brought about a shift in focus to rate cuts with market participants trying to predict when the first cut for various central banks is likely to take place. Initially, projections were for the Fed to start cuts in March with the market pricing in a greater than 70% chance although this has been tapered back to closer to 40%. Central bankers have maintained the view that they remain data dependent although some of the members are definitely more dovish than a few months ago which has resulted in positive market reaction. The path to rate cuts will still be influenced by the macroeconomic data and we believe the central banks will remain cautious on their cutting path as the worst scenario for them is if they cut early and inflation rears its head and they need to reverse path as this will raise questions around their credibility. For this reason, we believe rate cuts are more likely towards the middle of the year however as outlined by the chart on the next page there has been clear progress on bringing inflation back down to target so the view to rate cuts is a lot clearer than it was 6 months ago.

Measures of underlying inflation

Source: Bureau of Labor Statistics, Dallas Federal Reserve, New York Federal Reserve

As the market expected, the Fed kept rates on hold for the fourth consecutive meeting. What did draw the market’s attention was the commentary following the announcement with Chairman Powell maintaining his data dependence stance and emphasizing that there is still work to be done to get inflation to 2%. He further indicated that he does not see a rate cut taking place in March and the overall tone of the commentary was seen as more hawkish than the market expected.

Asset allocation

Our asset allocation remains in line with how we positioned at the end of 2023 and despite acknowledging some stocks have run hard our view is to remain in markets even with some anticipated volatility in the first half of the year as the second half could be rewarding but timing of markets is very challenging. We have upweighted our structured notes allocation slightly as a good way to add hedged equity to portfolios with a yield underpin. Finally, our bond holdings remain unchanged following our increased allocation at the end of 2023 which has performed well to date.

Market performance

January started off slowly with a negative trend following the strong end to 2023. Offshore markets then saw some positive momentum as goldilocks supportive data gave market participants confidence although there was a retracement at month end following hawkish comments from the Fed. Unfortunately the local market struggled to gain any positive moment. As per chart below the YTD performance of the JSE is -3.04%, while the S&P500 is up 1.73% and the World index is up 1.59%.

Indices Performance YTD

Equities

Earnings season kicked off with the banks where the initial reaction was slightly negative despite strong results. Some of the headwinds expected for the banking sector relate to a rate cutting environment’s impact on NII (net interest income). Airlines also came under pressure with specific focus on Boeing following a panel blowing off of a 737 Max mid-flight. TSM, a long term preferred stock of DI, had a strong start to the year following better than expected profits and projected 20%+ sales growth for 2024 which the market liked. We also saw strong results coming out of Microsoft and Google although market expectations were very high so the response was fairly muted despite beating consensus. As outlined by the chart below earnings expectations are high for 2024 following a low base in 2023, but this is sector specific as shown below.

The Magnificent 7 are still a key driver of the earnings outlook as highlighted by the charts on the right for both the final quarter of 2023 and moving into 2024. This helps validate the strong performance we saw in 2023 however it also means expectations are elevated especially looking at the benefit of AI coming through the income statement. We still have a very positive outlook on many of the Magnificent 7 but think a lot of good news has been baked into the price. Markets tend to overestimate the benefit of technology in the short term (AI) and under estimate in the long term so we can expect some volatility in the short term but the long term outlook remains positive.

The other important consideration is valuation. Looking at the chart on the right which is the forward PE of the S&P500 which we can see has run hard and is well above the average. This puts the index at risk of correction if earnings don’t hold up and hence why current earnings season guidance is being watched closely.

Bonds

Following the drop in yields towards the end of 2023 the movement has been largely sideways albeit with quite a bit of volatility. As indicated by the lower plot of the chart below the 2 year and 10 year have been following the same trajectory as the expectation for rate cuts has driven yields lower. However, it is important to note that the yield curve still remains inverted as indicated by the negative spread between the 2 year and 10 year which although narrowing has spent the last year in negative territory. This has historically been an indicator of a recession which the market is not currently paying attention to. We are comfortable with our bond positioning in portfolios – effectively locking in total returns of greater than 5% over the next 18-36 months. Yields remain attractive considering the pullback experienced last year.

Conclusion

From a macro perspective the environment looks more positive for 2024 but some of this good news has already been absorbed by the market in the year-end rally of 2023. Uncertainty remains around the timing of rate cuts and whether the projection of inflation is to remain in a clear disinflationary trend. Markets don’t operate in a straight line so we are expecting a bit of a bumpy first half of 2024 as these aspects are unpacked by markets. Should the data continue to trend in the right direction and the soft landing be achieved then we would expect risk assets to be rewarded in the second half of the year. For now it is important to remain in the market and manage positioning to benefit from the longer term expectations of risk asset returns which we still believe will be rewarding for our clients.

Download Full Investment Environment Article and Graphs (PDF, 800KB)