Markets in Flux: Shifting Sentiment in April 2026

Geopolitical tensions, volatile energy prices, and evolving policy signals kept investors on edge, even as resilience in economic data offered cautious optimism.

Introduction & Macro Overview

April marked a period of sharp transitions in market sentiment as investors navigated an evolving geopolitical backdrop, volatile energy markets and increasingly complex policy signals. The month opened under the weight of escalation in the Middle East, with renewed concerns around oil supply disruptions and their inflationary consequences. These developments reinforced a cautious tone across markets and prompted a renewed focus on downside risks. However, as April progressed, tentative diplomatic signals and a gradual stabilisation in energy prices helped ease some of the immediate fears, allowing markets to refocus on economic fundamentals and corporate earnings.

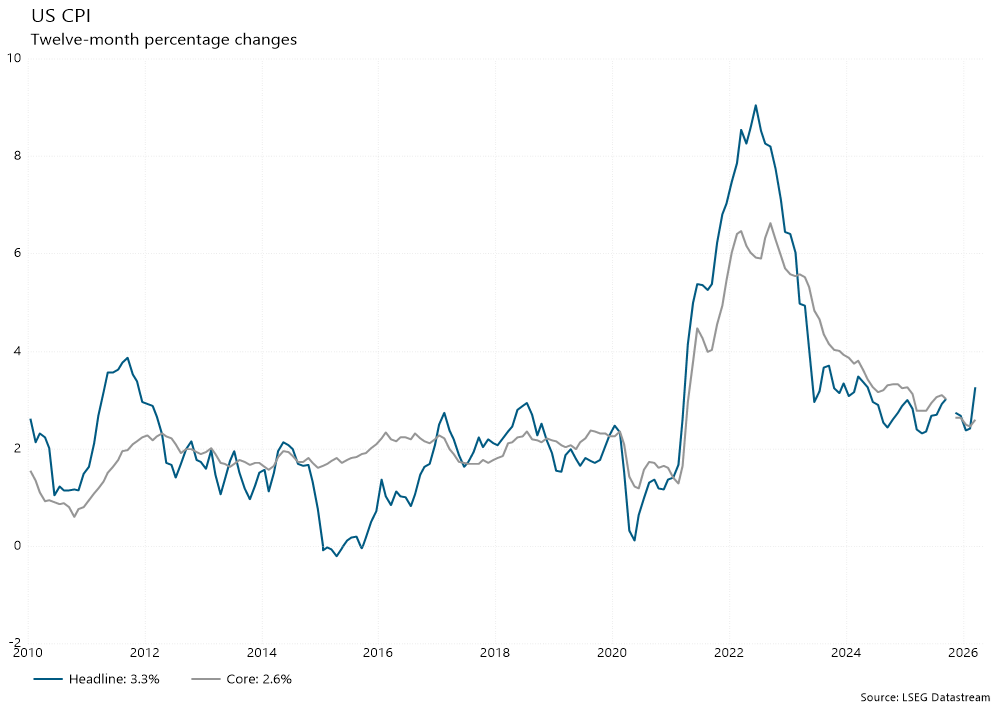

Economic data through the month remained mixed but broadly resilient. While inflation pressures re‑emerged through higher energy costs (see chart below), underlying growth indicators, particularly in the United States, continued to point to an economy slowing but not stalling. Labour market conditions softened modestly yet remained far from recessionary, and corporate results generally exceeded expectations. This combination supported a gradual improvement in confidence toward the latter part of the month, although investors remained acutely sensitive to headlines and policy messaging.

Monetary policy expectations shifted further during April. Central banks were forced to acknowledge that the path to policy easing would be slower and less predictable than previously anticipated. The persistence of inflation risks, compounded by geopolitical uncertainty, reduced the scope for near‑term rate cuts and reinforced a higher‑for‑longer narrative. As a result, asset prices oscillated between relief rallies and renewed caution, reflecting a market still searching for a durable equilibrium.

Geopolitical Developments and Energy Markets

Geopolitics remained the dominant macro driver throughout April. Early in the month, the intensification of conflict involving Iran raised the prospect of prolonged disruptions to global energy supply, particularly through the Strait of Hormuz. Oil prices responded swiftly, moving sharply higher and reintroducing acute concerns around energy‑driven inflation. The volatility in oil markets highlighted the fragility of global supply chains and the asymmetric risks embedded in current geopolitical conditions.

As the month progressed, diplomatic efforts and shifting rhetoric began to temper worst‑case assumptions. While the conflict remained unresolved, markets increasingly priced a lower probability of sustained supply outages. Oil prices pulled back from their peaks, albeit remaining elevated relative to earlier in the year. This moderation provided some relief for risk assets, but the episode reinforced how quickly inflation risks can resurface when geopolitical tensions intersect with constrained supply dynamics.

For policymakers, the energy shock further complicated an already difficult balancing act. Higher fuel costs fed directly into inflation expectations at a time when central banks were seeking confirmation that disinflation trends were durable. The result was increased caution in forward guidance and a reduced willingness to signal imminent easing, contributing to continued volatility across rates, currencies and risk assets.

Asset Allocation

Against this backdrop, asset allocation during April remained focused on risk management and resilience rather than aggressive return seeking. The elevated uncertainty around geopolitics and policy reinforced a preference for diversification and selective exposure. The moderation in oil prices allowed some risk assets to recover, but the wider environment did not provide enough comfort for the team to shift towards a risk on stance.

Equity allocation remained balanced, while our caution around fixed income remains. Hedged equity has provided some stability and overall portfolios are well balanced on a risk reward basis.

Market Performance

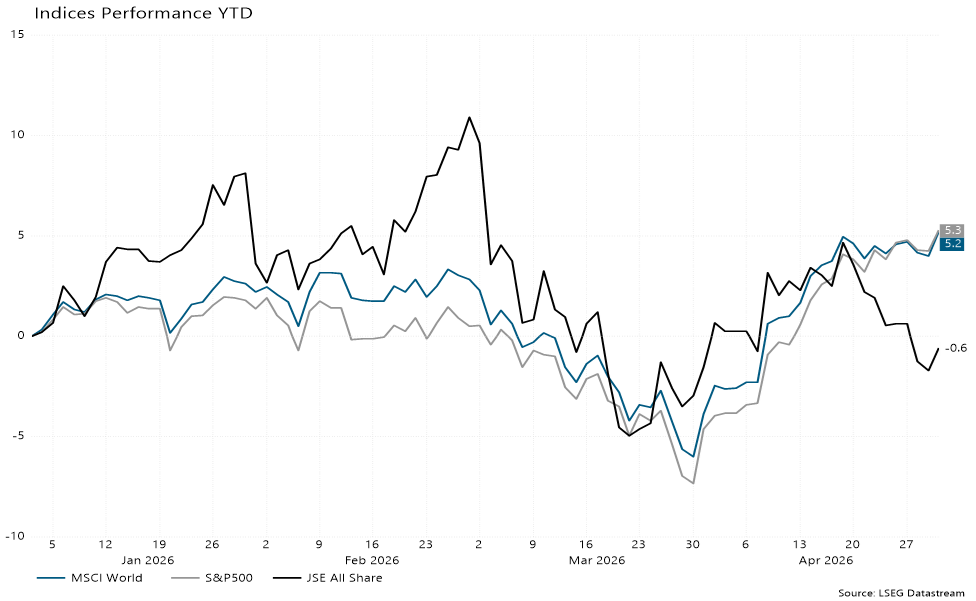

April saw global markets stage a strong recovery despite the uncertainty around the conflict in Iran. The JSE was up 0.98% in April while offshore markets saw the S&P500 up 10.42% and the MSCI World up 9.45%. As per the below chart the year to date performance for the S&P500 is up 5.3% (in USD) and the MSCI World is up 5.2% (in USD). Locally the JSE currently has a YTD performance of -0.6% (in ZAR).

Equities

Equity markets in April reflected a gradual shift from macro‑driven stress toward renewed focus on company fundamentals. Early in the month, heightened geopolitical risk and elevated energy prices weighed on sentiment, reinforcing concerns around input‑cost inflation, consumer affordability and margin sustainability. This resulted in periods of volatility and pronounced sector rotation. As the month progressed, however, fears of sustained energy supply disruption eased, allowing markets to stabilise and recover lost ground.

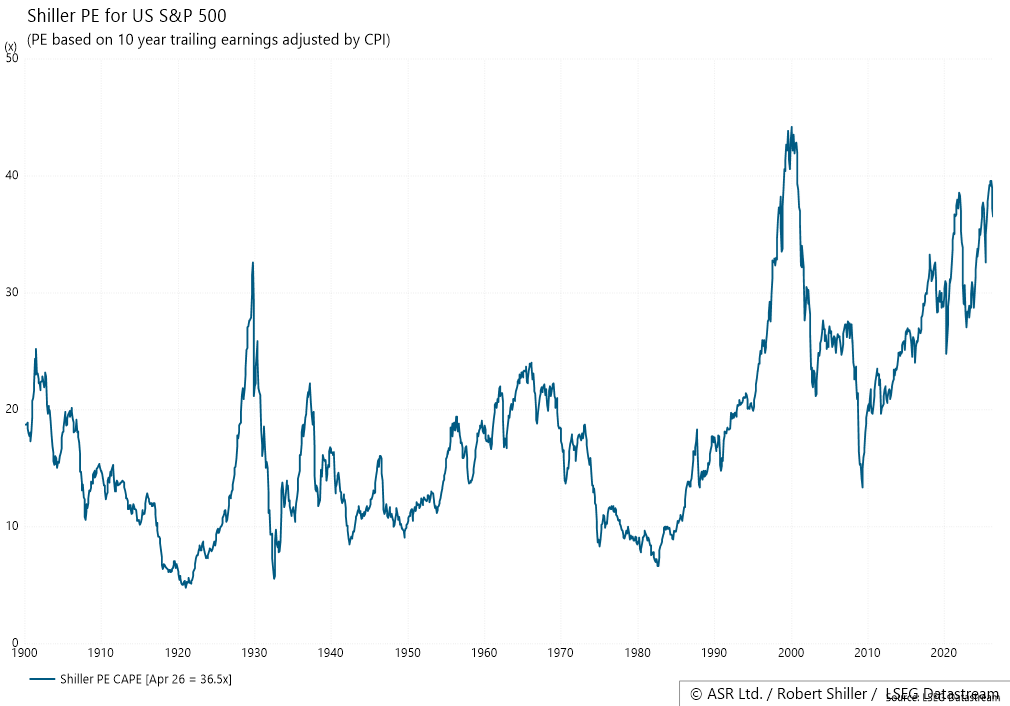

Corporate earnings played a central role in this transition. Results across several regions and sectors generally exceeded expectations, highlighting the ability of many companies to protect margins through pricing power, cost discipline and operational flexibility. Earnings resilience helped offset macro uncertainty and supported an improvement in risk appetite, particularly toward the latter part of the month. While more cyclical segments faced selective pressure, the broader earnings backdrop remained constructive. Earnings strength helps validate stretched valuations as per chart on next page.

Sector dispersion persisted throughout April. Energy‑related stocks benefited earlier from elevated oil prices, while defensive areas provided relative stability during periods of renewed stress. As sentiment improved, growth‑oriented sectors, including technology, regained momentum, supported by confidence in longer‑term secular themes. In contrast, consumer‑facing and rate‑sensitive sectors continued to experience headwinds as higher costs and tighter financial conditions weighed on demand and valuations.

Fixed Income

Fixed income markets remained under pressure throughout April as investors grappled with the renewed inflationary impulse stemming from higher energy prices and the resulting implications for monetary policy. While hopes for policy easing had featured prominently earlier in the year, developments over the past two months have reinforced a more cautious outlook. Central banks increasingly emphasised data dependency and downside inflation risks, pushing expectations for rate cuts further into the future and maintaining upward pressure on yields.

Sovereign bond markets experienced ongoing volatility, particularly at the longer end of yield curves. Periods of risk aversion and growth concern provided temporary relief rallies, but these were often short‑lived as inflation expectations reasserted themselves. The result was a challenging environment for duration‑heavy exposures, with investors adjusting to the prospect of policy rates remaining restrictive for longer than previously assumed. Yield curves reflected this uncertainty, oscillating between steepening on inflation fears and flattening as growth risks periodically resurfaced.

Conclusion

April highlighted the market’s ability to adapt to rapidly changing conditions, while also underscoring the fragility of sentiment in a world shaped by geopolitical risk and persistent inflation uncertainty. The recovery in risk assets toward the end of the month reflected confidence in underlying economic resilience, yet this confidence remains conditional and highly sensitive to external developments.

Looking ahead, markets are likely to remain volatile, with price action driven as much by geopolitical and policy developments as by economic data. In this environment, disciplined portfolio construction, diversification and a focus on quality remain essential. We continue to monitor developments closely, balancing caution with selective opportunities as markets navigate an uncertain but evolving landscape.

As always, we remain available to discuss portfolios or the broader investment environment in more detail.