March 2026 : Conflict involving Iran intensifying and energy markets reacting sharply

Once again we noticed how quickly market conditions can shift when geopolitical risks intersect with inflation dynamics.

Introduction & Macro Overview

March proved to be a month in which markets were once again reminded how quickly macro assumptions can be disrupted by geopolitical developments. After beginning the year focused on inflation normalisation and the prospect of gradual policy easing, investors were forced to reassess the outlook as the conflict involving Iran intensified and energy markets reacted sharply. The resulting rise in oil prices re‑introduced inflation risks that had been steadily fading, complicating the policy backdrop and driving a renewed period of volatility across asset classes.

Economic data over the month did little to suggest an abrupt deterioration in global growth. However, confidence was clearly dented as higher energy costs raised concerns about consumer purchasing power and the durability of disinflation trends. Market sentiment became increasingly headline‑driven, oscillating between risk‑off positioning during periods of escalation and tentative relief rallies when diplomatic efforts gained traction. While markets remained liquid and orderly, sensitivity to news flow increased meaningfully, reinforcing a cautious and selective investment environment.

In the United States, the combination of still‑resilient activity indicators and rising energy prices complicated the Federal Reserve’s task. Inflation progress appeared at risk of stalling should oil prices remain elevated, while consumer sentiment showed signs of strain. Elsewhere, policymakers faced similar trade‑offs, balancing the desire to support growth against the risk that renewed inflation pressures could become embedded. As a result, the global macro narrative shifted away from imminent easing toward a more uncertain and conditional outlook.

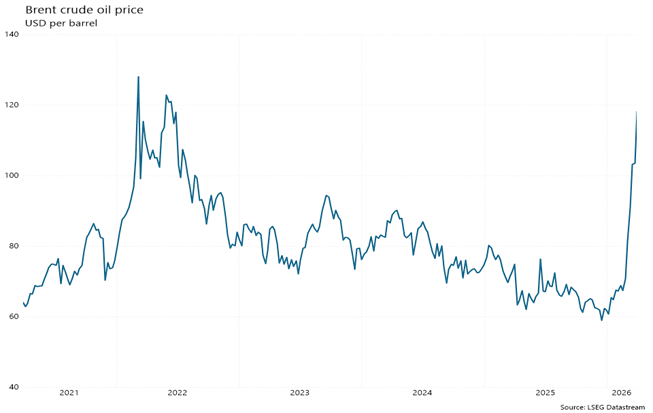

Market performance in March reflected the heightened uncertainty. Global equity markets experienced sharp swings, with periods of pronounced weakness interspersed with short‑lived recoveries. Commodity markets were a key driver, with oil prices surging (see chart below Brent Oil price) during episodes of escalation before retreating modestly as ceasefire discussions emerged. These moves had significant spill‑over effects across regions and sectors. Currency markets displayed a clear risk‑off bias. The US dollar strengthened against most major currencies, supported by safe‑haven demand and reduced expectations for near‑term policy easing. Emerging‑market currencies were more volatile, particularly those linked to energy imports, as higher oil prices threatened external balances.

Iran War

The escalation of the conflict between the US and Iran represents one of the most significant geopolitical shocks markets have faced in recent decades. What began as a targeted US‑Israeli military operation against Iranian nuclear and military infrastructure rapidly evolved into a broader regional confrontation, with material consequences for energy markets, global inflation dynamics and investor confidence. The situation remains fluid and has introduced a level of uncertainty that markets have been forced to price in quickly.

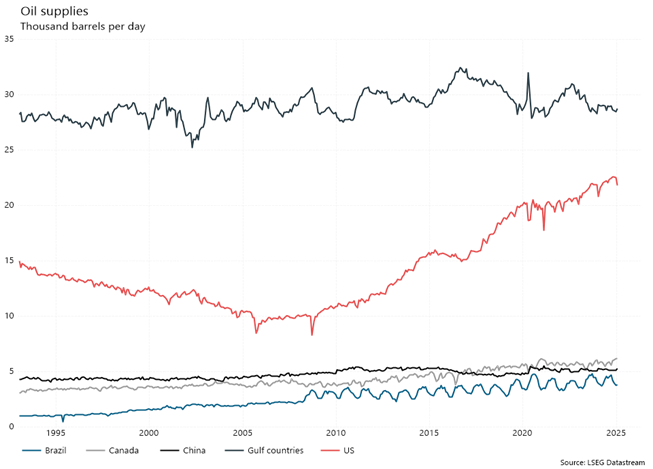

A key feature of the conflict has been its impact on global energy supply. Iran’s actions in the Persian Gulf, including the effective closure of the Strait of Hormuz, have disrupted a critical conduit for global oil and liquefied natural gas flows. This has resulted in a sharp spike in oil prices and heightened concerns about the durability of global supply chains (see chart below Oil Supplies). While partial retracements have occurred on hopes of diplomatic engagement and supply responses, energy markets remain sensitive, reflecting the scale and importance of the region to global energy security.

The macroeconomic consequences of this energy shock are inherently inflationary. Higher fuel and transport costs feed directly into consumer prices and production inputs, raising the risk that inflation proves more persistent than previously anticipated. This has complicated the outlook for central banks, which had entered 2026 expecting to normalise policy as inflation eased. Instead, policymakers are now balancing the risk of higher inflation against the possibility that prolonged disruption could weigh on growth, increasing the risk of stagflationary conditions in more energy‑dependent economies.

Financial markets have responded with a pronounced shift toward risk aversion. Equity markets have come under pressure, volatility has risen, and performance dispersion has increased across regions and sectors. Traditional safe‑haven dynamics have been mixed, reflecting the tension between higher inflation expectations and the demand for stability in uncertain conditions. Currency markets have favoured perceived safe havens, while emerging markets and energy‑importing economies have faced greater stress.

Looking ahead, the range of potential outcomes remains wide despite the news of a potential off ramp. A contained conflict that allows energy flows to normalise would likely limit the long‑term economic impact, while a prolonged or escalating confrontation would materially increase risks to growth, inflation and financial stability. In this environment, disciplined risk management, diversification and a focus on quality remain critical, as markets continue to navigate a landscape shaped as much by geopolitics as by traditional economic fundamentals.

Asset Allocation

Against this backdrop, asset‑allocation decisions in March were increasingly driven by risk control rather than return maximisation. The team has managed risk by tactically adjusting asset allocation back in October and we looked at further hedging in the current volatility by taking a long position in oil or down weighting equity depending on the portfolio. The renewed inflation risk also prompted a reassessment of interest‑rate sensitivity within portfolios. Fortunately, we have been under weight bonds which has provided some protection in this environment. Our hedged equity component of the portfolio is not immune to the market sell off but we see a smaller drawdown when compared to the market. In the local portfolios our Rand hedge bias has provided some protection from local market pressures. Overall portfolios have not escaped the selloff in March but have benefitted from some protection and proactive management.

Market Performance

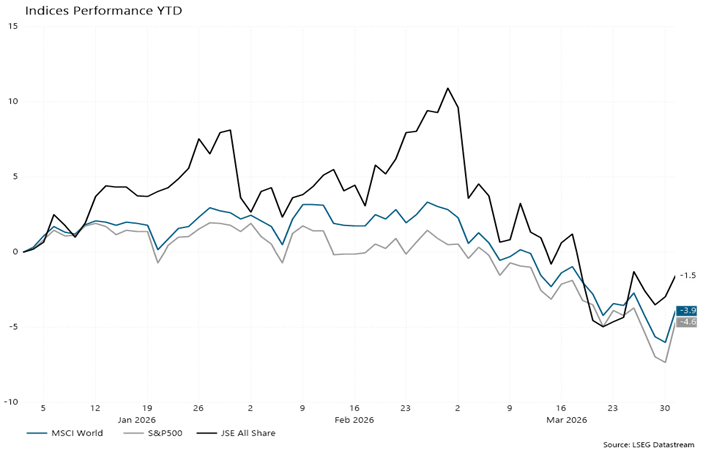

March saw global markets give back gains achieved this year. The JSE was down 11.2% in March while offshore markets saw the S&P500 down 5.09% and the MSCI World down 6.55%. As per the below chart the year to date performance for the S&P500 is down 4.6% (in USD) and the MSCI World is down 3.9% (in USD). Locally the JSE currently has a YTD performance of -1.5% (in ZAR).

Equities

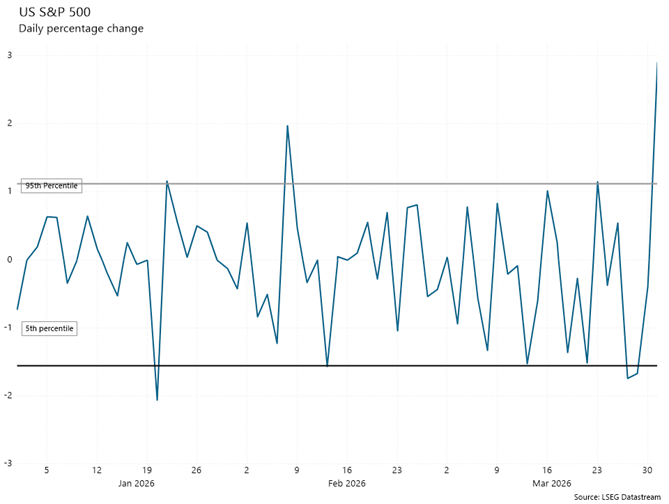

Equity markets in March were characterised by heightened volatility and increased dispersion beneath the surface. This is outlined in the chart below as we saw an increase in negative days. Energy‑related sectors benefited from higher oil prices, while more rate‑sensitive areas of the market came under pressure as discount rates moved higher. Consumer‑facing sectors were also challenged, reflecting concerns about the impact of rising energy costs on household spending.

Technology and growth stocks were particularly volatile. While long‑term structural themes remain intact, higher yields and uncertainty around the macro environment weighed on valuations. Investors became more discerning, differentiating between companies with strong balance sheets, pricing power and resilient earnings profiles, and those more exposed to cost pressures or slowing demand.

Despite the turbulence, markets continued to reward fundamental strength. Companies able to demonstrate earnings durability and strategic flexibility were better positioned, while speculative or highly leveraged business models struggled. This environment reinforced the importance of quality and active selection, rather than reliance on broad market momentum.

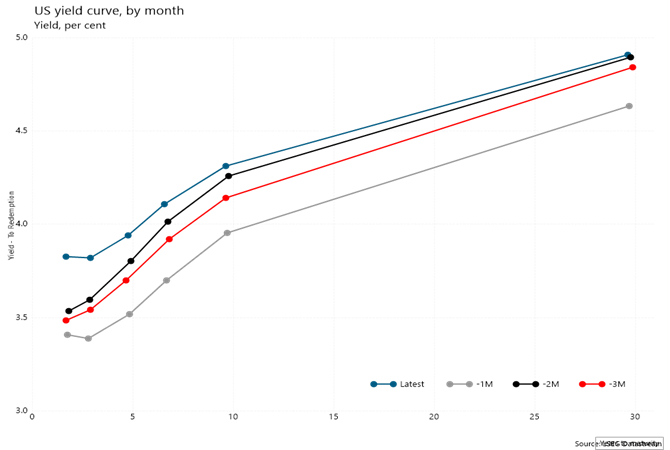

Fixed Income

March was a difficult month for fixed‑income markets globally. The sharp rise in oil prices and renewed inflation concerns pushed yields higher across major sovereign bond markets, resulting in meaningful losses. The sell‑off was most pronounced at the longer end of yield curves, reflecting concerns that central banks may be forced to maintain restrictive policy settings for longer than previously anticipated. This is highlighted in the US yield curves reflected by month on the next page.

Expectations for rate cuts were pushed further out, particularly in the United States and Europe, as investors reassessed the inflation outlook. Yield curves remained under pressure, and volatility increased as markets attempted to price the balance between slowing growth risks and inflation persistence. While bond markets remained functional, the margin for error narrowed as valuations adjusted to a more uncertain policy path.

Conclusion

March underscored how quickly market conditions can shift when geopolitical risks intersect with inflation dynamics. The resurgence of energy‑driven inflation concerns challenged the optimistic assumptions that had taken hold earlier in the year and forced investors to reassess both policy expectations and portfolio positioning. While there remains a credible path toward stabilisation should tensions ease and energy prices normalise, the month highlighted the fragility of sentiment and the speed with which volatility can return.

Looking ahead, markets are likely to remain sensitive to geopolitical developments, with price action driven more by headlines than by incremental economic data. In this environment, disciplined portfolio construction, diversification and prudent risk management remain paramount. We continue to monitor developments closely, balancing caution with a readiness to respond as opportunities emerge.

We recognise that periods of heightened uncertainty can be unsettling. Our focus remains on preserving capital, maintaining flexibility and positioning portfolios to navigate a wide range of potential outcomes. As always, we are available through the usual channels to discuss portfolios or the current investment environment in more detail.