Markets forced to reconcile in February 2026

Significant headlines drove heightened market volatility, with geopolitical developments in the Middle East introducing another layer of uncertainty.

Introduction & Macro Overview

February unfolded as a month in which markets were forced to reconcile strong underlying economic momentum with a renewed surge in geopolitical risk. Investors navigated a landscape shaped by resilient growth data, shifting expectations around central-bank policy, and a sharp escalation in Middle Eastern tensions following US and Israeli strikes on Iran. As in January, market narratives rotated frequently: optimism around disinflation and earnings durability competed with concerns about energy prices, rate volatility and the risk that geopolitical shocks could spill into inflation or growth outcomes. Markets remained functional and liquid, but sensitivity to headlines was elevated, reinforcing a more tactical and selective approach across asset classes.

In the United States, the dominant theme was the persistence of economic strength alongside a more cautious Federal Reserve. Labour-market data surprised meaningfully to the upside, reinforcing the view that the US economy remains fundamentally resilient despite higher interest rates. Employment gains were broad-based and unemployment edged lower, challenging expectations that tighter financial conditions would translate into a rapid slowdown. At the same time, inflation continued to trend lower, with both headline and core measures sitting at their lowest levels of the post-pandemic cycle. This combination of firm growth and easing inflation created a “Goldilocks” backdrop in theory, but in practice it complicated the Fed’s path forward.

The Federal Reserve’s decision to hold rates steady in late January was followed by a market reassessment of the timing and scale of future cuts. Strong employment data and firm activity indicators pushed expectations for rate easing further out, with investors increasingly accepting that the Fed is in no hurry to pre-commit to cuts while growth remains robust. This shift was amplified by political developments, notably the nomination of a more hawkish Federal Reserve chair, which injected additional uncertainty into the policy outlook. The result was a rise in Treasury yields and renewed volatility in rates markets, as investors balanced improving inflation dynamics against the risk that policy could remain restrictive for longer than previously assumed.

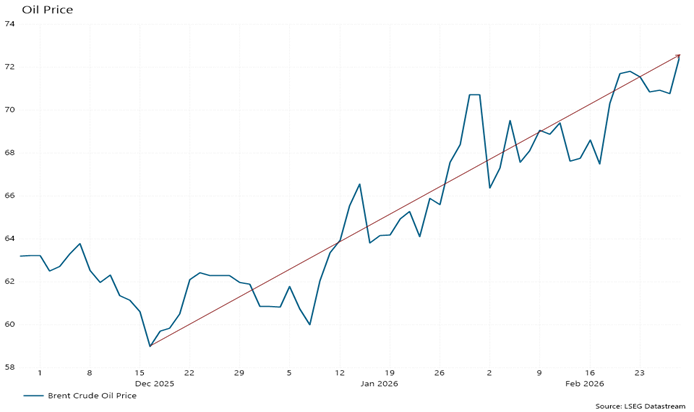

Geopolitical developments added a powerful new layer of complexity during February, centred on the escalation between the US, Israel and Iran. Markets reacted swiftly to the initial strikes, with oil prices jumping sharply (following a steady increase since December) as investors priced the risk of broader conflict and potential disruption to Middle Eastern supply routes. The focus quickly narrowed to the Strait of Hormuz, given its critical role in global energy flows. While fears of a full scale supply shock drove sharp short term volatility, markets appeared to oscillate between relief and renewed caution as the situation evolved. Oil prices, although off their peaks, remained elevated, underscoring persistent uncertainty around the risk of further escalation and the recognition that any miscalculation by Iran could still materially disrupt global energy markets.

Markets are still adjusting positioning in response to the shock, as investors weigh tail risks against the absence of immediate economic fallout. While the initial spike in oil prices may yet prove temporary, a sustained period of elevated energy costs would introduce a range of knock on effects that markets are unlikely to welcome. With sentiment remaining fragile and liquidity increasingly driven by key headlines, the coming week is expected to be bumpy, marked by elevated volatility and sharp, headline driven moves rather than a clear directional trend.

South Africa’s 2026 Budget struck a notably constructive tone, reinforcing the improving fiscal trajectory and supporting investor confidence. Delivered against a backdrop of stronger‑than‑expected revenue collection and narrowing deficits, the Budget avoided any broad‑based tax increases, with government withdrawing previously contemplated tax hikes and fully adjusting personal income tax brackets and rebates for inflation. For the first time in many years, the primary surplus (i.e. revenue less expenditure (excluding interest service costs) is growing resulting in public debt stabilising and beginning to decline as a share of GDP, while debt‑service costs are set to ease over the medium term—an important signal for long‑term interest‑rate stability. Increased infrastructure spending, improved fiscal credibility following South Africa’s exit from the FATF grey list, and the country’s first sovereign credit upgrade in over a decade further supported sentiment. While economic growth remains modest and structural challenges persist, the Budget was broadly well received by markets, reinforcing the rand’s resilience and underpinning local bond demand.

Asset Allocation

Our local portfolio allocation remains unchanged, as improving investor sentiment and business confidence continue to support an overweight position in equities. We have also maintained our bond exposure despite strong recent performance, reflecting its ongoing role in portfolio stability. Offshore, we have increased our equity allocation, as the recent sell‑off driven by AI‑related concerns appears overdone and has created attractive stock‑specific opportunities. At the same time, we remain mindful of the evolving geopolitical landscape and are cautious about making any significant portfolio shifts until greater clarity emerges. Against a backdrop of a constructive inflation outlook and an uncertain Federal Reserve path, we are also exploring additional bond exposure, while our hedged equity positions continue to underpin portfolio growth.

Market Performance

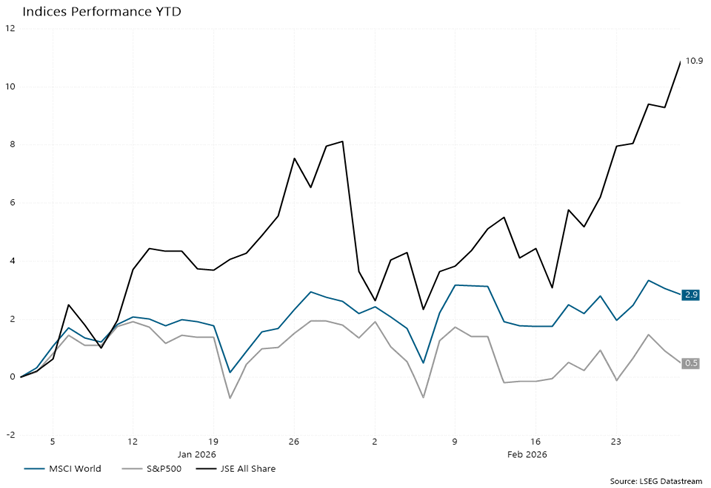

January saw markets start the year on the front foot despite all the volatility. The JSE produced 7% in February while offshore markets were more muted with S&P500 down 0.87% and the MSCI World up 0.18%. As per the below chart the year to date performance for the S&P500 is up 0.5% (in USD) and the MSCI World is up 2.9% (in USD). Locally the JSE currently has a YTD performance of 10.9% (in ZAR).

Fixed Income

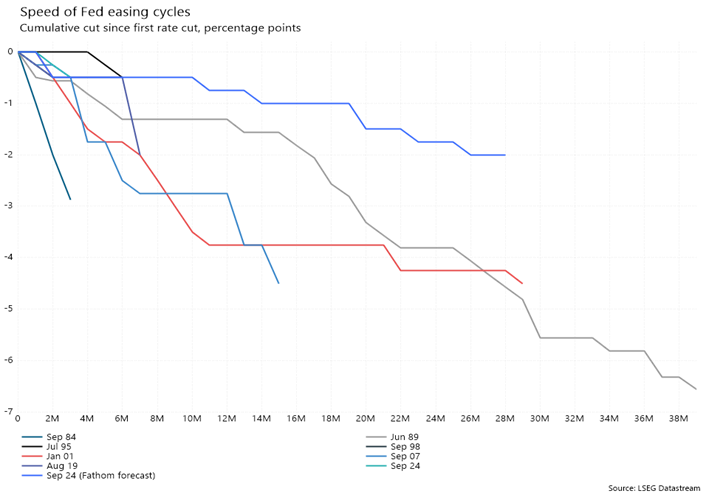

Rates markets reflected the push and pull between strong data and policy uncertainty. US yields moved higher as expectations for near-term rate cuts were pushed out, while yield curves remained relatively flat. Volatility was most pronounced at the long end, where fiscal concerns, supply dynamics and geopolitical risk premiums intersected. In contrast, UK and South African yield curves were comparatively stable, reflecting more anchored inflation expectations and steady central-bank messaging. The anticipated path of the Fed easing cycle is still uncertain and as outlined by the chart below it has followed a slower trajectory than past cycles. Overall, fixed-income markets remained functional, but the margin for error narrowed as investors demanded clearer confirmation that inflation is sustainably under control.

Equity markets in February were characterised by increased dispersion beneath the surface, with pockets of pressure emerging even as broader indices remained range‑bound. A notable theme was the sharp underperformance of many software‑as‑a‑service (SaaS) companies, as investors reassessed business models in light of rapidly advancing generative AI capabilities. Concerns grew that AI could compress pricing power, shorten product cycles or allow larger platforms to internalise functionality that had previously supported standalone software revenues. This triggered a swift de‑rating across parts of the SaaS universe, particularly among companies with premium valuations and less defensible competitive moats. Against this backdrop, Nvidia’s earnings were once again a focal point for markets. While results confirmed extraordinary demand for AI‑related hardware and continued revenue momentum, the market reaction was more nuanced than in previous quarters. Shares were volatile as investors weighed exceptional near‑term growth against already elevated expectations, intensifying scrutiny on sustainability, customer concentration and the pace of capital expenditure across the AI ecosystem.

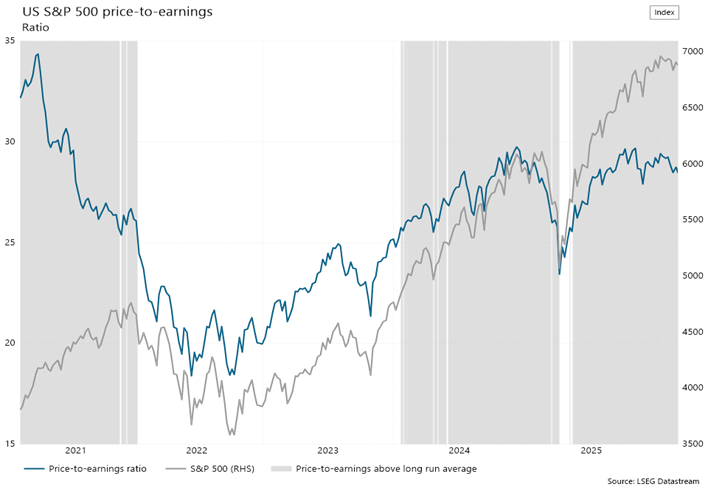

As illustrated in the following chart, equity valuations have spent an extended period running above long‑term averages, a trend largely justified by strong and sustained earnings growth. Where that growth outlook begins to change, valuation corrections can be swift and meaningful. However, a number of companies have been swept up in a broader negative news cycle despite fundamentals that remain intact, and it is precisely this disconnect that is starting to create selective opportunities.

Conclusion

February was marked by significant headlines that drove heightened market volatility. Recent geopolitical developments in the Middle East have introduced another layer of uncertainty, something markets are inherently uncomfortable with. While there are tail risks that, if realised, could place sustained pressure on markets and potentially weigh on global growth, there is also the possibility that a rapid de‑escalation limits the impact to a short‑lived disruption within broader macro trends. We recognise that this uncertainty can be unsettling, and we want to reassure clients that the team is closely monitoring developments, with a strong focus on prudent risk management while remaining alert to emerging opportunities. As always, we are available through the usual channels should any client wish to discuss their portfolio or the current environment in more detail.

Download Investment Environment Article (PDF, 605KB)