Crisis management to cautious optimism in June 2026

Although the conflict in Iran remains central, investors are becoming more comfortable with their view on outcomes.

Introduction & Macro Overview

June represented a meaningful shift in the global investment landscape as markets transitioned from a period dominated by geopolitical escalation to one increasingly focused on resilience in economic activity, corporate earnings and structural investment themes. While conflict involving Iran remained a central feature throughout much of the month, investors became progressively more comfortable with the view that the worst-case outcomes for global energy markets were unlikely to materialise. This change in sentiment contributed to a strong recovery in risk assets and allowed equity markets to finish the first half of the year on a very positive note.

Economic data remained supportive. The United States continued to display resilience through relatively healthy labour market conditions, stable consumer confidence and ongoing corporate profitability. At the same time, inflation remained above central bank targets, creating an environment where policymakers remained cautious. Markets therefore found themselves balancing encouraging growth dynamics against the prospect that interest rates may remain elevated for longer than previously expected.

One of the defining characteristics of June was the continuing dominance of artificial intelligence as a market theme. Large-scale investment commitments to semiconductor manufacturing, data centres and digital infrastructure accelerated globally. While this supported corporate earnings expectations and equity valuations, it also intensified debate around whether current levels of spending can ultimately generate economic returns sufficient to justify the scale of capital being deployed.

Monetary policy remained a key focal point. The Federal Reserve maintained policy rates but adopted a noticeably more hawkish tone as inflation concerns persisted. The combination of resilient growth and lingering inflation pressures resulted in markets steadily adjusting to a scenario where policy easing remains further away than many investors had hoped at the start of the year.

Geopolitical Developments and Energy Markets

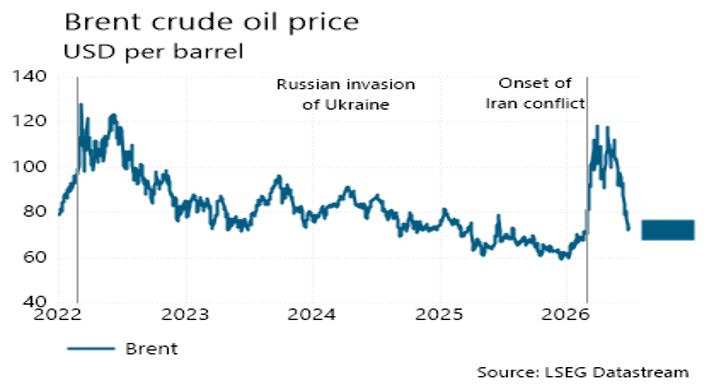

Following several months of elevated geopolitical tensions and supply disruptions centred around the Strait of Hormuz, progress toward a ceasefire between the United States and Iran began to restore confidence that global energy flows would normalise. While negotiations remained fragile and periodic tensions persisted, markets increasingly priced in a lower probability of prolonged supply disruptions.

This shift had immediate implications for oil markets. Crude prices declined sharply during the month as shipping routes gradually reopened and concerns around supply shortages eased. By month end, oil prices had largely returned to levels seen before the most severe phase of the conflict, helping reduce one of the most important inflationary pressures facing the global economy. The speed with which energy markets adjusted demonstrated that investors were increasingly focused on medium-term supply fundamentals rather than short-term geopolitical headlines.

The decline in oil prices provided meaningful support to financial markets. Lower energy costs improved the outlook for consumers and businesses while reducing fears of a sustained inflation shock. However, policymakers remained cautious, recognising that the inflationary effects of earlier energy price increases may still take time to work through the global economy. As such, while the direction of travel improved significantly, the interaction between energy markets and inflation remained an important risk factor going forward.

Asset Allocation

The improvement in market sentiment and easing of energy-related risks created a more constructive investment backdrop during June. Nevertheless, portfolio construction continues to emphasise diversification and disciplined risk management. While the probability of a severe energy-driven economic slowdown has reduced, valuations in several areas of the market have become increasingly demanding and market leadership remains relatively concentrated.

Equity allocations remain balanced with a preference for quality businesses capable of delivering sustainable earnings growth. Exposure to structural growth themes, including artificial intelligence, remains important, although increasing attention is being given to valuations and position sizing. Fixed income allocations remain below long-term strategic targets as inflation uncertainty and hawkish policy signals continue to create an uneven risk-reward profile for longer-duration bonds.

Market Performance

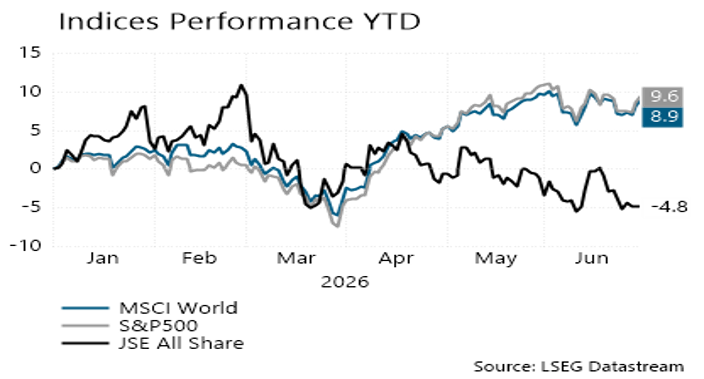

June saw a slight negative move in offshore markets despite some risks abating. The JSE was down 3.7% in June while offshore markets saw the S&P500 down 1% and the MSCI World down 1.2%. As per the below chart the year to date performance for the S&P500 is up 9.6% (in USD) and the MSCI World is up 8.9% (in USD). Locally the JSE currently has a performance of -4.8% (in ZAR).

Equities

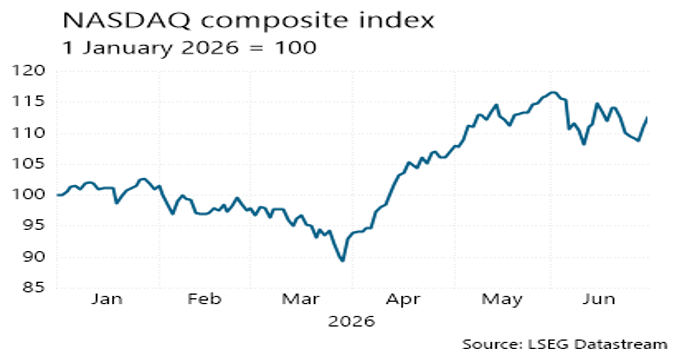

Equity market performance during June was overwhelmingly driven by earnings expectations and continued enthusiasm around artificial intelligence. Technology companies, semiconductor manufacturers and businesses linked to digital infrastructure continued to attract significant investor interest as capital expenditure plans expanded globally. Major investment programmes announced in Asia, combined with continued spending by large US technology companies, reinforced confidence in the long-term growth potential of the sector.

Corporate earnings generally remained supportive. Investors increasingly looked through geopolitical volatility and focused on the ability of businesses to grow revenues and maintain margins despite ongoing inflation pressures. Improved confidence regarding the energy outlook further supported risk appetite and allowed equity valuations to remain elevated.

Despite this positive backdrop, several risks remain. Valuations have expanded further, market leadership remains concentrated and questions are growing regarding the long-term economic return on enormous AI-related infrastructure spending. Markets are therefore increasingly dependent on continued earnings execution to justify current pricing levels. While the investment case for artificial intelligence remains compelling, investors should remain mindful that periods of strong thematic enthusiasm often create pockets of excess optimism.

Fixed Income

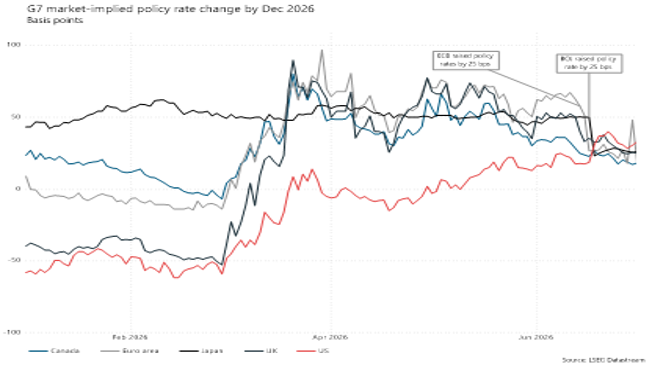

Fixed income markets continued to navigate a challenging environment throughout June. Falling oil prices provided some relief by easing inflation concerns, but this was partially offset by resilient economic data and increasingly hawkish central bank communication. Investors therefore continued to adjust expectations toward a higher-for-longer interest rate regime.

Government bond markets experienced periods of stability as energy prices declined, but yields remained elevated by historical standards. Markets remained particularly sensitive to labour market data, inflation releases and Federal Reserve commentary. The prospect that inflation may remain above target while growth continues to hold up has limited the case for meaningful duration exposure.

We therefore continue to believe that caution is warranted within fixed income portfolios. While income yields have become increasingly attractive, the balance between inflation risk and policy uncertainty suggests that selectivity remains important.

Conclusion

June marked a transition from crisis management toward cautious optimism. The reduction in geopolitical risks, improvement in energy markets and continued strength in economic activity provided a constructive backdrop for investors. Equity markets responded positively, supported by strong earnings and ongoing enthusiasm around artificial intelligence and digital infrastructure investment.

Looking ahead, investors must balance this improving backdrop against several important risks. Inflation remains above target, central banks continue to adopt a cautious stance and equity valuations have moved higher. Furthermore, while the AI investment cycle remains a powerful long-term theme, expectations have become increasingly ambitious and will require sustained earnings growth to justify current market pricing.

In this environment we continue to favour a disciplined and diversified approach, balancing participation in long-term growth opportunities with prudent risk management. While the outlook has improved meaningfully compared with earlier in the year, maintaining portfolio resilience remains essential as markets navigate the second half of 2026.