Resilient Markets in May 2026

Markets were supported by strong earnings while central banks remained cautious, with rate cuts pushed out and a higher-for-longer interest rate environment increasingly priced in.

Introduction & Macro Overview

May extended many of the themes that emerged in April, with markets continuing to navigate a complex intersection of geopolitical risk, resilient growth dynamics and persistent inflation pressures. The month was characterized by a notable divergence between strong asset price performance and an underlying macro environment that remains fragile.

Geopolitical tensions in the Middle East continued to dominate the backdrop, particularly through their impact on energy markets (high oil) and inflation expectations. At the same time, global economic activity showed continued resilience, led by the United States, where consumer demand and corporate earnings remained supportive. This combination sustained risk appetite, although market sentiment remained highly sensitive to changes in inflation data and policy expectations.

Monetary policy remained firmly in focus throughout May. While central banks largely maintained current policy settings, the prospect of near-term rate cuts continued to recede. Sticky inflation and elevated energy prices reinforced a cautious stance, with markets increasingly adjusting to a higher-for-longer interest rate environment.

The earnings season particularly around AI remained very strong and this was a key tailwind for market. Specifically, semiconductors have benefitted from the current capex outlook and across the board we are seeing outsized returns. We have seen a significant rotation back into technology and this is driving the S&P500 to new all-time highs. We face an interesting environment where technological revolution in the form of AI is driving very positive sentiment and a lot of hype. While we like this theme and think there are some strong underlying fundamentals, this sort of behavior also should be met with some skepticism and hence we are spending significant time on risk management. There is also significant excitement around the SpaceX IPO which is something we will be watching closely in June.

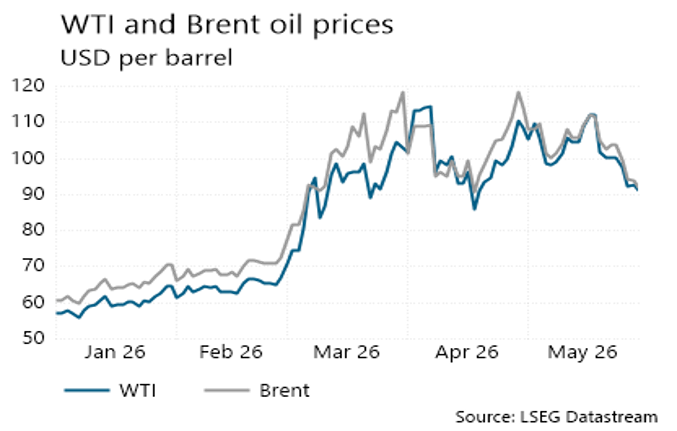

Geopolitical Developments and Energy Markets

Geopolitical risk remained elevated throughout May, with ongoing tensions in the Middle East continuing to influence global markets. While there were intermittent signs of diplomatic engagement, uncertainty around the durability of any resolution persisted. This contributed to continued volatility in energy markets and reinforced the importance of geopolitical developments as a key driver of macro conditions.

Oil prices remained elevated during the month, reflecting ongoing supply constraints and disruptions to key transport routes. Although prices fluctuated in response to shifting headlines, the overall level remained sufficient to sustain upward pressure on inflation. The persistence of higher energy costs continued to feed into broader price expectations, complicating the outlook for central banks and financial markets alike.

From a policy perspective, the energy backdrop reinforced caution. The risk that elevated fuel costs could translate into broader inflationary pressures limited the scope for policy easing and increased sensitivity to inflation data releases. As a result, markets remained reactive, with both risk assets and bond markets responding quickly to developments in oil prices and geopolitical sentiment.

Asset Allocation

In this environment, portfolio positioning remained anchored in diversification and risk management. While the strength in equity markets presented opportunities, the underlying macro risks warranted a measured approach.

Equity exposure remained balanced, with an emphasis on quality and resilience, while caution within fixed income persisted given the continued pressure on yields. Hedged equity strategies continued to provide stability within portfolios, supporting overall risk-adjusted returns.

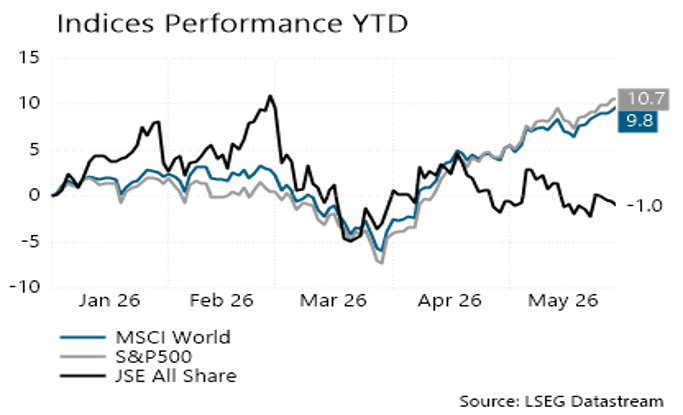

Market Performance

May saw continued strength in markets as investors looked through the macro backdrop. The JSE was down 0.48% in April while offshore markets saw the S&P500 up 5.15% and the MSCI World up 4.37%. As per the below chart the year to date performance for the S&P500 is up 10.7% (in USD) and the MSCI World is up 9.8% (in USD). Locally the JSE currently has a YTD performance of -1% (in ZAR).

Equities

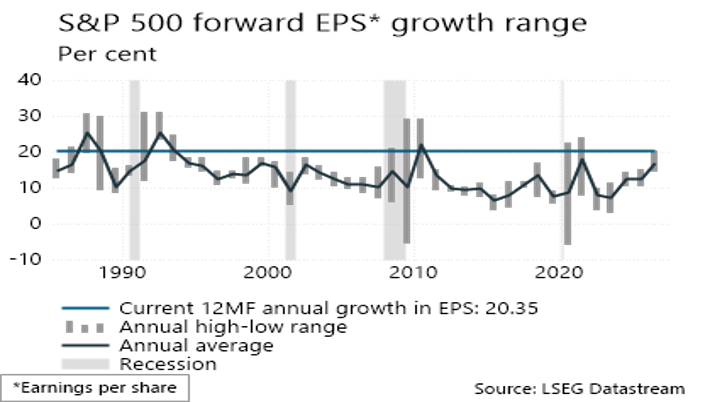

Equity markets in May were driven primarily by corporate fundamentals, with earnings continuing to exceed expectations (see chart on next page) across a broad range of sectors. The strength of earnings growth, combined with sustained investment in technology and infrastructure, supported positive sentiment and further gains in global equities.

Technology and growth-oriented sectors remained key leaders, benefiting from continued investment linked to artificial intelligence and digital infrastructure. This thematic support has become an increasingly important driver of market performance, offsetting broader macro concerns.

Despite the positive backdrop, underlying risks remain. Market leadership has been relatively concentrated, and valuations in certain segments have expanded, leaving markets sensitive to shifts in interest rate expectations or earnings outlooks. Consumer-facing sectors and more rate-sensitive areas continued to experience mixed performance, reflecting the ongoing impact of higher borrowing costs and inflation pressures.

The strong performance has been underpinned by great earnings but we believe the equity market is currently looking through a lot of the macro risk. This will only be possible if we see some normalization in the short term. If the uncertainty around Iran and the knock on effect from elevated oil and other commodities persists we can expect a tipping point where those risks will outweigh the strong earnings. Prediction and timing is impossible and so we maintain a balanced approach.

Fixed Income

Fixed income markets continued to face headwinds during May as inflation remained elevated and expectations for policy easing were pushed further out. Bond yields remained volatile, with upward pressure reflecting both inflation concerns and the resilience of economic activity.

While periods of risk aversion provided temporary support for sovereign bonds, these moves were generally short-lived. The broader environment remains challenging for duration exposure, with central banks showing limited urgency to ease policy in the near term.

Yield curves continued to adjust to this backdrop, reflecting a balance between persistent inflation risks and the potential for slower growth over time. As such, fixed income markets remain highly sensitive to incoming inflation data and central bank communication. For this reason we remain underweight our normal bond exposure as we think the risks and rewards are not currently balanced.

Conclusion

May reinforced the key themes shaping the current investment environment: resilient economic growth, elevated geopolitical risk and persistent inflation pressures. While equity markets have continued to perform strongly, this strength masks a more complex and uncertain macro backdrop.

Looking ahead, the interaction between energy markets, inflation and monetary policy will remain central to market direction. While the global economy continues to demonstrate resilience, the margin for error has narrowed, particularly in the context of elevated valuations and tighter financial conditions.

In this environment, maintaining a disciplined and diversified approach remains essential. We continue to balance participation in equity upside with careful risk management, focusing on quality assets and resilient portfolio construction as markets navigate an evolving and uncertain landscape.