Resilient markets in spite of persistent global uncertainty in November 2025

Macroeconomic forces, policy shifts, and sector-specific developments shaped investor sentiment and asset performance.

Introduction & Macro Overview

November 2025 unfolded against a backdrop of persistent global uncertainty, yet markets demonstrated notable resilience. The month was marked by a complex interplay of macroeconomic forces, policy shifts, and sector-specific developments that shaped investor sentiment and asset performance.

The U.S. economy remained a focal point, with the Federal Reserve’s policy path under intense scrutiny. Early in the month, optimism grew as the U.S. government appeared poised to end its historic shutdown, which had delayed the release of key economic data and injected volatility into both equity and fixed income markets. As the shutdown resolution neared, the Dow Jones Industrial Average closed at record highs, while the Nasdaq lagged due to a pullback in AI-related stocks. The S&P 500 and global indices reflected a cautious optimism, buoyed by robust earnings from technology giants and ongoing enthusiasm for artificial intelligence and cloud infrastructure.

Monetary policy remained a central theme. The Federal Reserve maintained a data-dependent stance, with policymakers signaling that further rate cuts would be contingent on incoming economic data. The delayed release of inflation and labor market figures due to the shutdown left markets and the Fed “flying blind” for much of the month. Nevertheless, as data trickled in, it became clear that the labor market was softening, with private employers shedding jobs and unemployment ticking higher. This, combined with subdued inflation readings, fueled market speculation about a potential rate cut in December. Treasury yields fluctuated in response, with the 10-year yield hovering near 4.1%.

Globally, central banks in major economies adopted a cautious tone. The European Central Bank and Bank of England held rates steady, while Japan’s central bank hinted at a possible rate hike, contributing to policy divergence. In emerging markets, policy responses varied, but prudence prevailed as authorities weighed inflation risks against the need to support growth.

Trade policy and geopolitical developments continued to influence sentiment. The U.S. and China made incremental progress on tariff negotiations, and the possibility of the U.S. allowing Nvidia to sell advanced AI chips to China signaled a friendlier approach after a recent trade truce. As shown by the chart on the next page import prices in the US are ticking up. Meanwhile, supply chain disruptions, such as the global recall of Airbus A320 jets and a major fire in Hong Kong, underscored the fragility of interconnected markets. In commodities, oil prices were volatile, buffeted by U.S. sanctions on Russia, OPEC+ supply adjustments, and ongoing geopolitical tensions. Gold prices surged at times, reflecting safe-haven demand amid market jitters.

In South Africa, the economic environment remained relatively stable. The South African Reserve Bank cut its policy rate, reflecting confidence in the country’s inflation trajectory and the relative stability of the rand. Local bonds continued to attract investor interest, with yields easing slightly. The JSE extended its strong year-to-date performance, supported by sector rotation.

Corporate activity was robust, with notable deals in the technology and healthcare sectors. Amazon’s $38 billion cloud services agreement with OpenAI and Microsoft’s $9.7 billion data center deal with IREN highlighted the ongoing race for AI infrastructure. In healthcare, Eli Lilly became the first drugmaker to reach a $1 trillion market capitalization, driven by explosive demand for weight-loss drugs.

Overall, November’s macro environment was defined by a delicate balance between optimism and caution. While markets showed resilience in the face of persistent uncertainty, the outlook remained clouded by risks ranging from policy shifts and trade tensions to sector-specific challenges and questions about the sustainability of recent rallies. As we saw an uptick in volatility we are comfortable with our more cautious positioning into 2026 as there is a lot for the market to digest both on a macro level and company specific.

Asset Allocation

Our asset allocation strategies in November reflected a more defensive posture, shaped by the evolving risk landscape. Offshore equity exposure was trimmed in October, as the team judged that downside risks in global markets were not fully priced in and that much of the positive news had already been reflected in valuations. While portfolios retained upside participation through direct holdings and structured notes, a greater emphasis was placed on hedging to protect capital. Fixed income allocations remained unchanged, with a wait-and-see approach regarding inflation risks.

Locally, there was a modest upweighting of South African assets where appropriate, reflecting confidence in the domestic bond market’s compelling yields and the relative stability of the macroeconomic environment. The overall approach was one of prudent risk management—recognizing that while markets have delivered better-than-expected returns, it is critical to safeguard client capital as momentum can shift quickly. This cautious stance was further justified by the ongoing volatility in global markets, the uncertain trajectory of monetary policy, and the potential for renewed geopolitical or trade-related shocks.

Market Performance

November saw markets struggling for direction as macro events as well as bubble talk saw volatility pick up. The S&P500 was up 0.13% for the month, while the MSCI World was up 0.01%. The JSE was up again producing 1.51% for November. As per the below chart the YTD performance for the S&P500 is up 16.5% (in USD) and the MSCI World is up 18.6% (in USD). Locally the JSE currently has a YTD performance of 31.9% (in ZAR).

Fixed Income

The fixed income landscape in November was shaped by a convergence of monetary policy uncertainty, shifting investor sentiment, and evolving fiscal dynamics. U.S. Treasury yields remained volatile, with the 10-year yield oscillating around 4.1% as markets digested the Federal Reserve’s signals and the impact of the government shutdown. The delayed release of key economic data created a sense of unease, but as figures emerged, it became clear that the labor market was softening and inflation pressures were moderating. This fueled speculation about a potential rate cut in December, though Fed officials remained cautious, emphasizing the need for more data before committing to further easing. The 10-year yield is on a downward trajectory as per the chart on the next page but the path of the Fed remains uncertain.

Corporate bond issuance was robust, as companies sought to secure funding ahead of potential market turbulence. Notably, major technology firms turned aggressively to the debt markets to finance large-scale AI infrastructure investments, with public bond issuance by leading cloud and AI companies reaching nearly $90 billion since September. This surge in corporate borrowing raised concerns about the sustainability of debt-financed growth in the tech sector and the potential for strains in the corporate bond market, even as leverage across most major companies remained low for now.

Globally, central banks maintained a cautious stance. The European Central Bank and Bank of England held rates steady, while Japan’s central bank signaled a possible rate hike, contributing to policy divergence. In Canada, stable inflation readings led the Bank of Canada to signal a halt in rate cuts, with local bonds responding positively to the benign inflation outlook.

In South Africa, the fixed income market benefited from a stable policy environment and a benign inflation outlook. The South African Reserve Bank’s decision to cut 25bps reinforced confidence in the country’s inflation trajectory. Local bonds responded positively, with yields easing slightly and the SA 10-year government bond yield continuing its gradual decline. This environment supported the attractiveness of local fixed income assets for both domestic and international investors.

Overall, fixed income markets navigated a delicate balance between opportunity and caution, shaped by evolving monetary policy, fiscal dynamics, and shifting investor sentiment. The outlook remained uncertain, with vigilance warranted as new risks and opportunities continued to emerge.

Equities

Equity markets in November demonstrated remarkable resilience, building on the strong performance seen in October. The S&P 500 and Nasdaq posted gains, driven by robust corporate earnings and ongoing enthusiasm for technology and artificial intelligence. Amazon’s landmark $38 billion deal with OpenAI and Microsoft’s $9.7 billion data center agreement with IREN underscored the sector’s momentum, even as debates about bubble risks intensified.

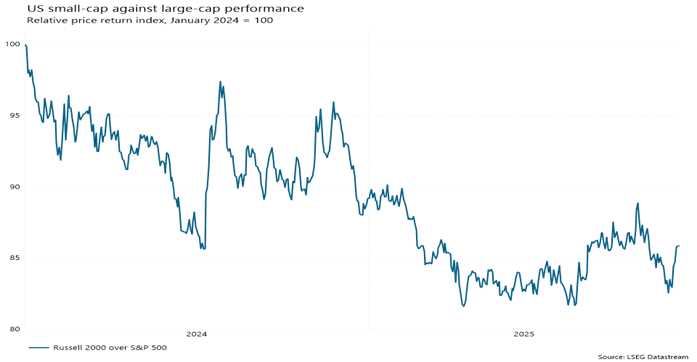

However, the AI-driven rally showed signs of strain, with volatility revealing cracks in the sector’s momentum. SoftBank’s $5.8 billion sale of its Nvidia stake stoked fears that valuations in the AI industry might have outpaced fundamentals. Meanwhile, concerns grew about the sustainability of debt-financed AI investments, as major tech firms turned to the bond markets to fund large-scale infrastructure projects. Despite these headwinds, investor appetite for risk assets remained strong, and the market’s “don’t fight the Fed and don’t fight AI” mantra prevailed. Sector rotation was evident as investors looked beyond technology stocks for new opportunities. As seen by the chart below the Russell 2000 outperformed the S&P 500 as allocators adjusted positioning. Healthcare emerged as a standout, with Eli Lilly becoming the first drugmaker to reach a $1 trillion market capitalization, driven by explosive demand for weight-loss drugs. In South Africa, the JSE maintained its impressive year-to-date trajectory, supported by both local and global factors.

Overall, equity markets reflected a delicate balance between optimism and caution. While the AI and technology sectors continued to drive gains, concerns about valuations, debt-financed growth, and sector-specific risks underscored the need for active management and vigilant risk assessment as the year draws to a close.

Conclusion

November 2025 saw markets remain resilient despite global uncertainty and policy shifts. Asset allocation was defensive, with a focus on risk management and capital preservation. While technology and AI drove gains, volatility and valuation concerns persisted. A cautious, flexible approach remains essential as risks and opportunities continue into 2026.

At DI we have been pleased with our positioning throughout the year and will be happy with a stable month in December to close out the year. We wish our clients a good Festive Break as we anticipate a busy year in 2026. Although the office will be closing on 19th of December and reopening on 5th January all portfolio managers will be available should clients need anything over the festive season.